ProfitShare in practice

To give you an idea of the difference ProfitShare could make, let's introduce you to Harry.

Harry has just joined his employer's pension plan.

- He’s decided to contribute £350 each month

- The monthly pension contribution will increase by 3.5% per year

- He’ll transfer £10,000 from a previous pension into his employer’s pension plan

- He’s aged 45

- He wants to retire at age 65.

Harry also has an existing Royal London Stocks and Shares ISA.

- He transfers £25,000 from an existing stocks and shares ISA into his Royal London Stocks and Shares ISA

- We've assumed his current ISA has no funds in it before transferring

- We've assumed he'll contribute £50 to his ISA each month

- The monthly ISA contribution will increase by 3.5% per year.

The amount Harry’s able to build up by age 65 depends on how his chosen investments perform each year, as shown in the example below.

Harry's pension and ISA projected values at age 65

These figures aren't guaranteed and are just an example. Harry could get more or less than this.

We've assumed he'll increase his pension and ISA contributions in line with inflation each year and that he'll contribute until he retires at age 65. We’ll apply an annual management charge of 0.40% to his pension and ISA.

We've assumed that inflation will reduce the buying power of Harry's pension and ISA by 2% each year. We've allowed for this by reducing the growth rate to 2.8%. This should give a more realistic view of what Harry could buy with his investments if he took his benefits today.

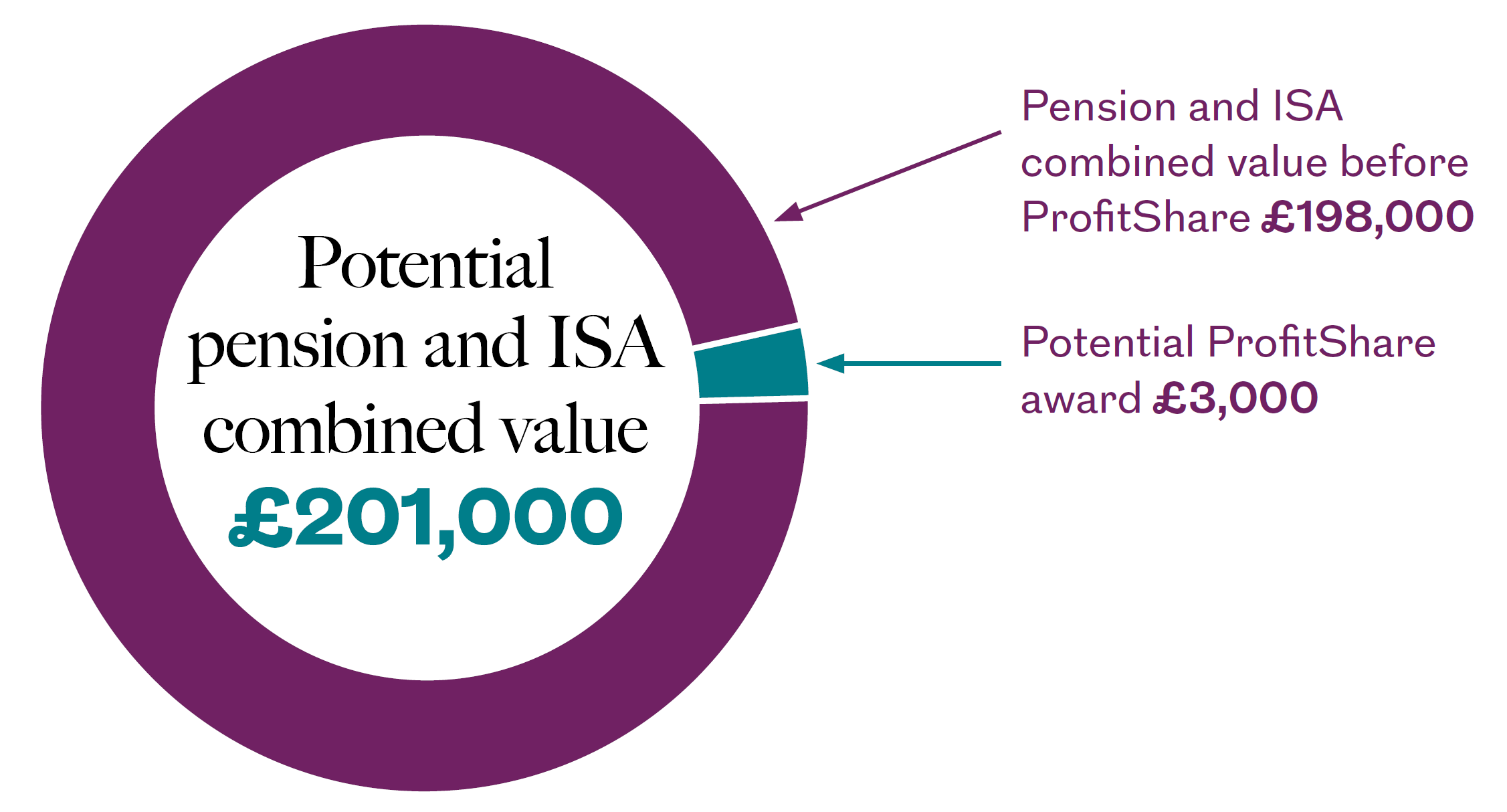

The impact of ProfitShare for Harry

Now let's look at the difference ProfitShare could make to Harry's pension and ISA savings, assuming we award 0.15% of the value of his plan each year and his investments grow by 2.8% each year.

These figures show that over time, ProfitShare could help to increase Harry's pension and investments from £198,000 to £201,000 giving him an extra £3,000.

You should remember that this is only an example and investment returns are never guaranteed. This means that while there's a chance your savings could grow, they could also fall in value. So you could get back less than you started with.

More about ProfitShare

Learn how ProfitShare works and how it could make a difference for you