-

Make sure your personal details and contact information are all up to date

-

Nominate or update your beneficiaries, so you don't leave your pension to the wrong person

-

Don't miss out on any potential extra retirement income and track down any lost pensions

-

Build your knowledge with our pension guides, to help understand what pensions are, how they work and how to get the most out of them

Pension Awareness 2025

We're delighted to be an ambassador for Pension Awareness 2025.

Pension Awareness isn't for one week of the year. From pension basics to finding out how your pension is invested, you can pay your pension some attention all year round with the free resources on their site.

Visit the Pension Awareness website

Check in on your pension

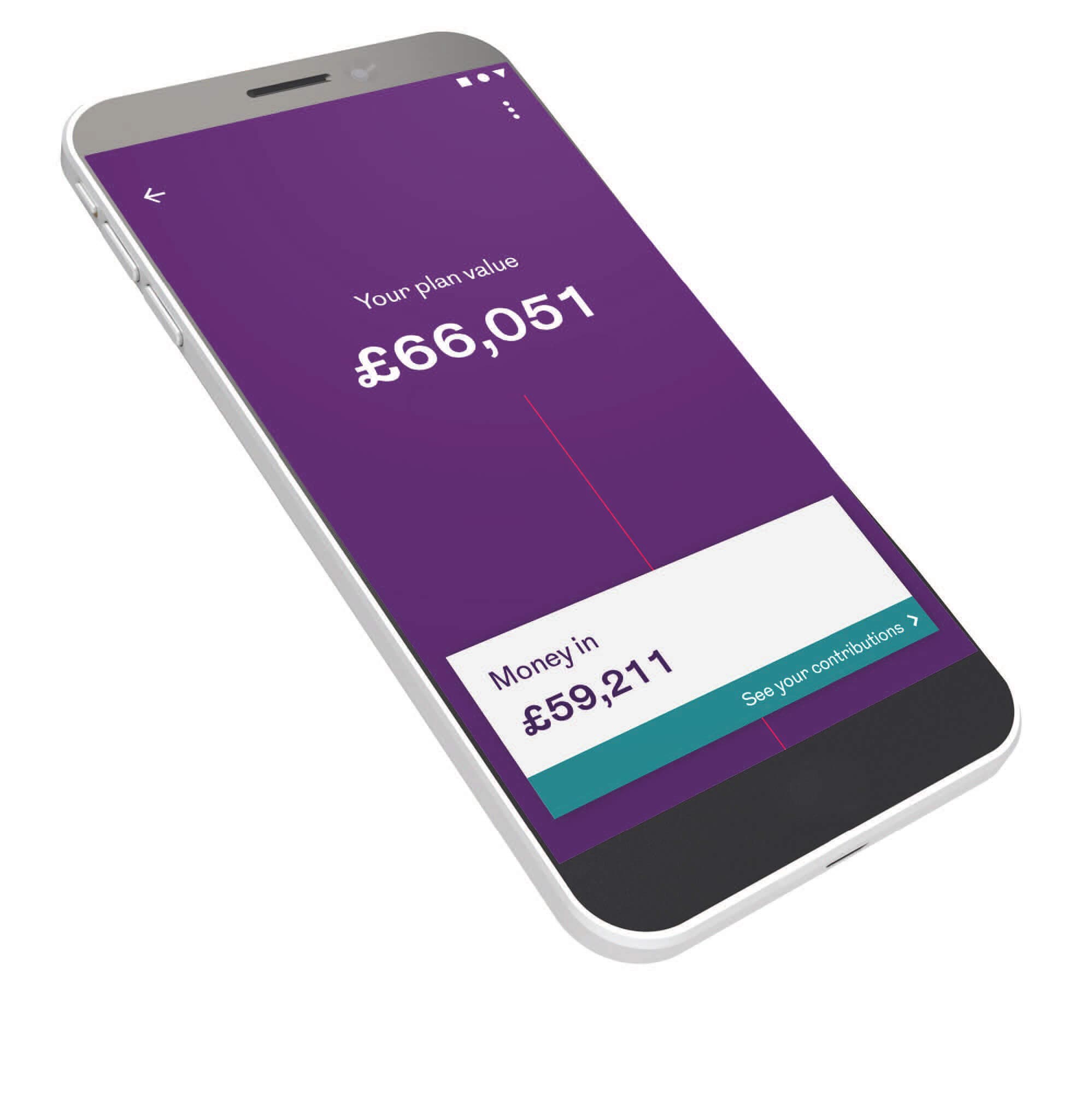

One of the easiest ways to give your Royal London pension some attention is to check it regularly using our mobile app. Available for Royal London pensions taken out since 2004 or with Scottish Life, it gives you quick and easy access to check in on your pension whenever you need.

Our 2025 Pension Awareness show and other webinars

In September 2025 we took part in one of the Pension Awareness Week live shows. Hosted by pension expert Clare Moffat and Consumer Finance Specialist Sarah Pennells, 'Your pension made simple' covered some pension basics, like how a pension works, pension contributions and salary exchange, and what you can be doing to make sure you're on the right track for retirement.

We also put together regular pension webinars of our own, so whether you want to know how to achieve a good income in retirement or how your pension's invested, our webinars can help you understand more.

You can catch up on all our webinar and Pension Awareness show recordings now.