Share

'Will we ever summit the Pension Mountain?' - New analysis from Royal London

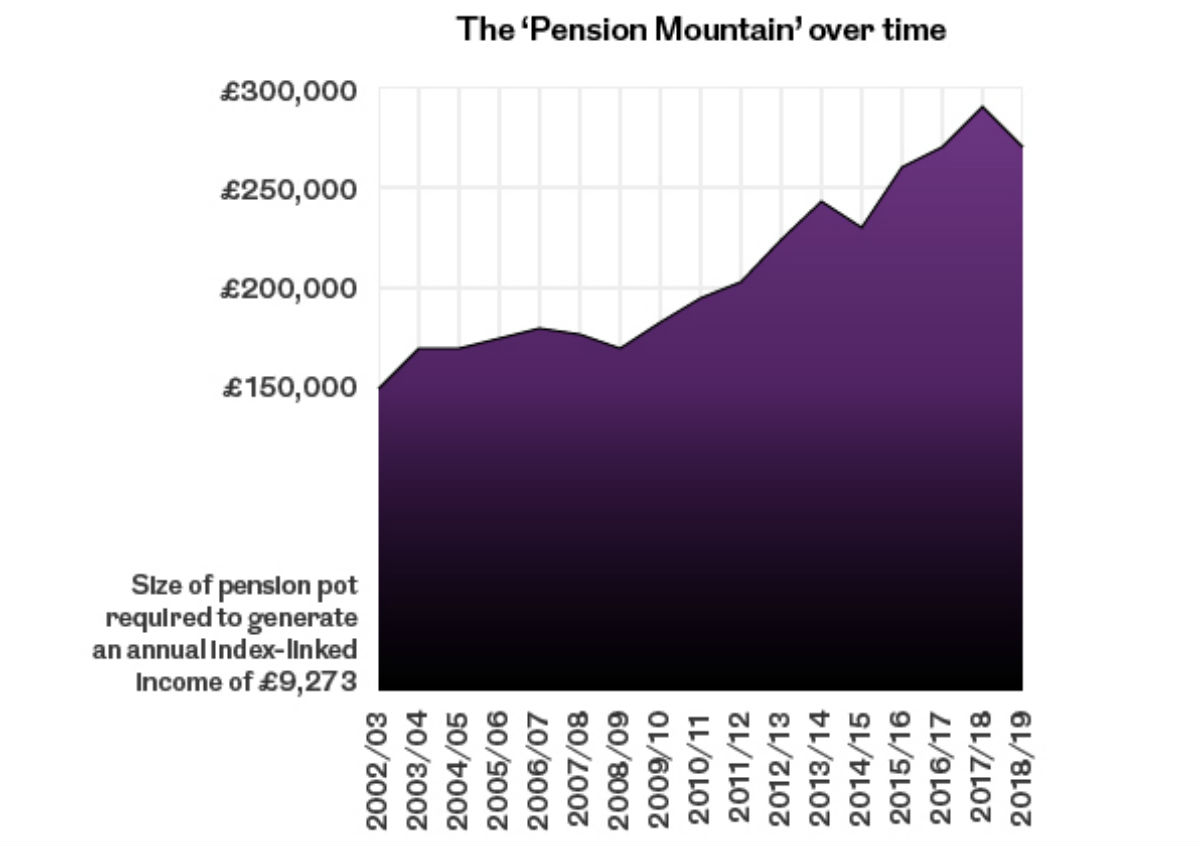

New research by mutual insurer Royal London has found that the pension pot needed to avoid an uncomfortable retirement – dubbed the ‘pension mountain’ – has grown in size in real terms by three quarters since 2002 from around £150,000 to £260,000. More worryingly still, falling levels of home ownership mean that younger generations who end up having to pay rent in retirement could need a total pot as high as £445,000 to avoid a slump in living standards when they stop work.

Royal London’s new policy paper – ‘Will we ever summit the Pension Mountain?’ – seeks to answer the most frequently asked question in pensions – how much do I need to save for my retirement? It looks at an average earner on just under £27,000 per year and assumes that they draw a full state pension of just over £8,500 per year. It assumes that retirement will bring some cost savings such as no longer having to pay a mortgage, no longer having to contribute into a pension and no work-related costs such as season tickets etc., and therefore suggests that workers who can retire on two thirds of their pre-retirement wage will see no fall in their standard of living when they stop work. This means a private pension income of just over £9,000 is needed in addition to the state pension.

Back in 2002/03, when interest rates were much higher and life expectancy was lower, a pension pot of around £150,000 would have delivered a private pension at this level through retirement. But as the chart below shows, the pension mountain has grown since then to stand at roughly £260,000 today.

As well as looking back, the paper also looks forward to an era when fewer people will have become home owners during their working life and more will have to fund a rent out of their retirement income. For the minority of pensioners who will be renting from a local authority or housing association, this means an extra £125,000 will be needed in pension saving to generate an income sufficient to cover ongoing rent in retirement. But for the growing number of pensioners renting from a private landlord, higher private rent levels mean a total pot of £445,000 will be required - £185,000 more than for someone who has no rent or mortgage costs in retirement.

Commenting, Helen Morrissey, Personal Finance Specialist at Royal London said:

"This research is a reminder that when we save for retirement we are chasing a moving target. If our retirement pot is going to support us through a longer retirement and in an era of lower interest rates, we are going to need to build a much bigger pot than in the past. More worrying still, we can no longer assume that we will be mortgage-free homeowners in retirement. For those unable to get on the property ladder during their working life, a large private rental bill needs to be factored in to retirement planning. For all of these reasons, we cannot afford to be complacent about current levels of retirement saving. This research also has big implications for the mandatory 8% contribution rate from April 2019 for those who have been enrolled into a workplace pension. This is a great start, but the government needs to act quickly to nudge people up to more realistic savings levels. Without this, many millions of people will face a sharp drop in living standards when they retire."

- ENDS -

One of the most frequently asked questions in the world of pensions is ‘how much do I need to put into my pension?’. The answer obviously depends on things like how old you are, how much you earn, when you plan to stop work and what standard of living you want in retirement. But one way of answering this question, as explored in this policy paper, is to think about the pension ‘pot’ that you need to have built up by the time you retire.

For further information please contact:

Helen Morrissey, Personal Finance Specialist, Royal London

- Email: helen.morrissey@royallondon.com

- Tel: 07919 170 712

Emily Horton, Press Officer, Royal London

- Email: Emily.horton@royallondon.com

- Tel: 07919 170 647

Note to editors

1. Here you can find the Royal London Policy Paper 21, ‘Will we ever summit the pension mountain?’

2. Recent research published by the Resolution Foundation suggested that around 1 in 3 of the ‘Millennial’ generation could find themselves renting ‘from cradle to grave’.

About Royal London:

Royal London is the largest mutual life, pensions and investment company in the UK, with funds under management of £117 billion, 8.8 million policies in force and 3,745 employees. Figures quoted are as at 30 June 2018.